- Posts

- 800

- Likes

- 722

Hands90

·BriteCo - DavidSW - Watch Insurance

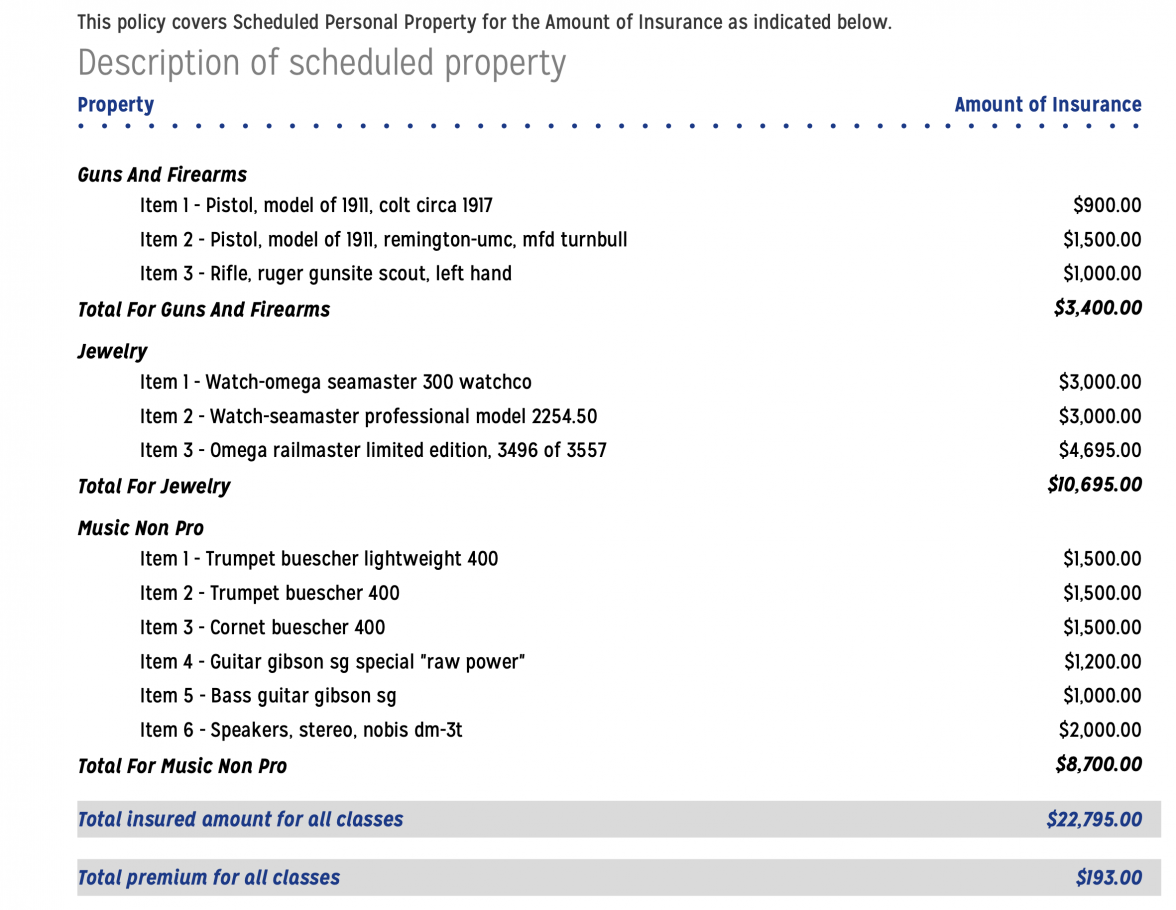

Never have I really looked into wrist watch insurance. I pay around $100 a year for my wife's ring through Jewelers Mutual but since I just bought my Grail watch through DavidSW, they sent me a link for BriteCo.

There is no reason not to do it other than if there is an issue and they do not resolve it.

Here is what they sent me

Here are the top five reasons to insure your jewelry with BriteCo:

I've owned Rolex Sub's and never thought about Insurance but now it seems like maybe I should be insuring my watch. Honestly it sounds too good to be true.

So I'm at the airport and my watch is stolen at security or it somehow ends up in a trash bin and they will just refund me?

Sorry to sound like an idiot but I never needed to work with an insurance company for a claim before.

Never have I really looked into wrist watch insurance. I pay around $100 a year for my wife's ring through Jewelers Mutual but since I just bought my Grail watch through DavidSW, they sent me a link for BriteCo.

There is no reason not to do it other than if there is an issue and they do not resolve it.

Here is what they sent me

Here are the top five reasons to insure your jewelry with BriteCo:

- Safe and secure with AM Best A rated insurance carrier

- Zero-deductible standard policy

- Full replacement if lost, stolen, or damaged up to 125% of appraised value

- Annual insurance value updates (no need to reappraise your jewelry)

- Fast, easy claim service using your local jeweler

I've owned Rolex Sub's and never thought about Insurance but now it seems like maybe I should be insuring my watch. Honestly it sounds too good to be true.

So I'm at the airport and my watch is stolen at security or it somehow ends up in a trash bin and they will just refund me?

Sorry to sound like an idiot but I never needed to work with an insurance company for a claim before.